In this article, we take a look at Kuwait’s fintech and wider digital ecosystem to see how things are developing.

Economic development strategies have been implemented across much of the Middle East and Africa (MEA) and this also includes Kuwait. Kuwait Vision 2035 will aim to diversify Kuwait’s economy and also help the country be less-oil reliant, which for most of the previous century until today has boosted the country’s economic development and its other Gulf Cooperation Council (GCC) neighbours.

Over 50 per cent of Kuwait’s population fall between the 15 to 39 years age group. In addition, 70 per cent of those who fall under the age group of 15 to 24 years old have a banking relationship, which is much higher than the 33 per cent average for the Middle East and 54 per cent globally.

According to Hootsuite, in terms of percentage of the population aged 15 and over, nearly 80 per cent has an account with a financial institution, almost a quarter has a credit card, and over a third makes online purchases and/or pays online bills. Like in the rest of the world during the height of the 2020 pandemic, Kuwaitis also went digital and their activities there increased dramatically. For instance, online banking usage was at 84 per cent during the pandemic. And in terms of perceived readiness to digital transformation, 80 per cent in Kuwait felt the government and telecommunications providers felt they were ready to shift to online services.

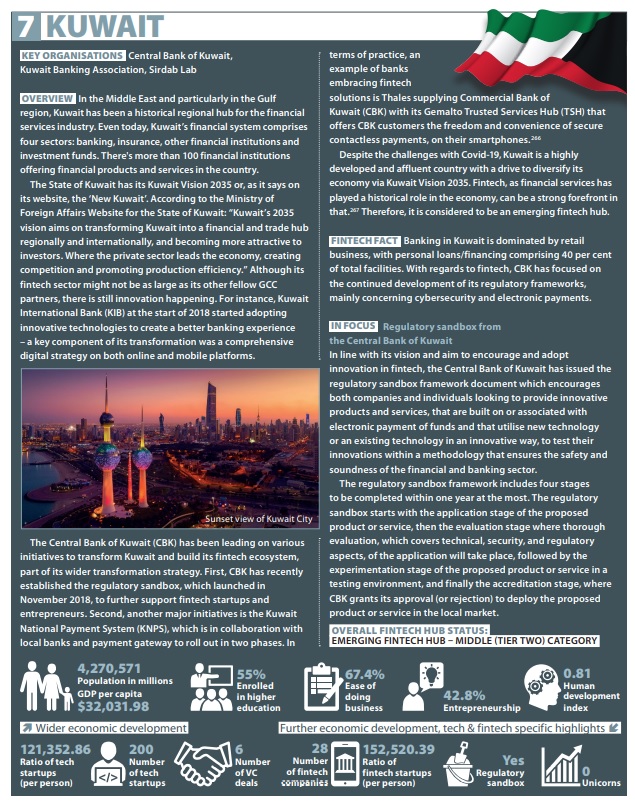

In the Middle East and particularly in the Gulf region, as highlighted in The Fintech Times Fintech: Middle East and Africa 2021 Report, Kuwait has been a historical regional hub for the financial services industry. Even today, Kuwait’s financial system comprises four sectors: banking, insurance, other financial institutions and investment funds. There were over 100 financial institutions offering financial products and services in the country. Banking in Kuwait is dominated by retail business, with personal loans/financing comprising 40 per cent of total facilities.

Also, Kuwait has produced some of the regions most iconic tech companies, such as delivery app Talabat and e-commerce platform Boutiqaat.

Due to its historical financial services ecosystem in the region coupled with the high economic development of the country and support from the top – coupled with a young and tech savvy population, fintech has potential to grow in Kuwait.

This has seen the government trying to drive much of the fintech developments in the country. This has seen, for example, the Central Bank of Kuwait (CBK) launch its regulatory sandbox back in November 2018. Also, in the following year when the government launched a $200million fund for investment in technology. This has also seen a fintech unit in the CBK going live as well and acknowledging that fintech is a priority for them. With regards to fintech, CBK has focused on the continued development of its regulatory frameworks, mainly concerning cybersecurity and electronic payments.

Last August, the CBK launched the new Kuwait Automated Settlement System for Interparticipant Payments (KASSIP). The new KASSIP system offers several advantages related to ensuring the security and smoothness of payment and settlement transactions and to liquidity management as well as allowing banks to issue reports on and monitor payment settlements through a designated electronic platform.

Also, the new system enables all local payment and transfer transactions among banks operating in Kuwait and to customers’ accounts to go through within seconds, and also enables instantaneous settlement of banks’ daily balances, according to the Arab Times.

Partnerships between banks and fintechs are also happening in Kuwait. The Oxford Business Review highlighted the following:

- Kuwait Finance House and National Bank of Kuwait (NBK) partnering with blockchain specialist Ripple and Gulf Bank using biometric facial recognition on its mobile app

- Kuwaiti fintech companies, such as secure payments brands Tap Payments and MyFatoorah, as well as real-estate-focused Ajar Online demonstrate the significant potential of the local landscape

- NBK launched its personalised investment app called NBK Capital SmartWealth service

- Boubyan Bank announced a new smartwatch payment system

In addition, NBK also launched its first digital bank Wayay, which is Kuwait’s first fully digital bank for youth. Also, NBK’s Group Digital Office, which acts as an Innovation Lab for NBK, comprising Digital Office and Digital Factory under one umbrella, acts as an accelerator. It recently won the ‘Best Financial Innovation Lab in Kuwait for 2022′,

Also, last year, Boubyan Bank, the leading Islamic bank based in Kuwait, signed a landmark agreement with Dubai International Financial Centre’s DIFC FinTech Hive to launch the ‘Boubyan Bank Accelerator Programme’,

In terms of how financial technologies are being used in Kuwait, according to Statista it highlights that peer-to-peer (P2P) money transfer had the highest adoption in Kuwait at under 50 per cent (44 per cent). In second place it was accounts aggregation at 17 per cent. In third place is a tie between connected home insurance and crowdfunding at 9 per cent. Finally, in fourth place is connected health at eight per cent.

Despite its success so far, more can be done and fintech can further grow. However, despite a lower adoption of fintech compared to its other GCC neighbours, 83 per cent of Kuwaitis are willing to adopt fintech solutions. Also, as mentioned with the previous examples of youth and startup empowerment such as the accelerators, future Kuwaiti entrepreneurs and residents can further one day create their own fintech businesses.

On a final note, key players in the wider Kuwaiti fintech ecosystem include of course the Central Bank of Kuwait as well as the Kuwait Banking Association, Capital Markets Authority, Insurance Regulatory Unit – to name a few.

Kuwait’s future looks to grow with digital transformation and sectors like fintech helping lead that charge.